Apple: DOJ Antitrust Lawsuit – Potential Fallout, Upcoming GenAI Supercycle – Cyber Tech

Anna Moneymaker/Getty Photographs Information

Have you ever missed the boat on Apple Inc. (NASDAQ:AAPL)? AAPL has been a inventory which has seemingly soared increased and better despite perennially buying and selling at wealthy valuations. The inventory’s voracious run, nonetheless, has hit a bit of a pause because it is likely one of the lone mega-cap tech titans which continues to commerce under all-time highs. The inventory has gone nowhere ever since 2021, and this underperformance might have created a lovely shopping for alternative. In the meantime, the Division of Justice (‘DOJ’) is ready to lastly launch its antitrust lawsuit in opposition to the corporate, which can rattle traders already involved with the valuation. On this report, I clarify why I’m upgrading the inventory on account of a possible generative AI supercycle, as I anticipate the corporate’s long-term monitor report of execution will outweigh any potential fallout from antitrust proceedings.

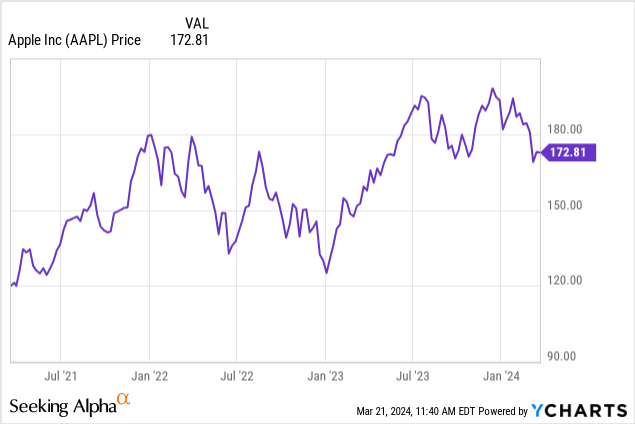

AAPL Inventory Worth

I final coated AAPL in September the place I defined why I used to be downgrading the inventory attributable to valuation and potential geopolitical dangers. The inventory has since underperformed the broader market by round 20%.

That underperformance has made the inventory considerably extra enticing than earlier than from a valuation perspective, and I’m coming to understand the potential delayed increase as the corporate finally cashes in on generative AI.

DOJ To Launch Antitrust Lawsuit In opposition to Apple

The DOJ is predicted to sue AAPL for violating antitrust legal guidelines as quickly as Thursday. This lawsuit is predicted to result in a hefty effective and potential enterprise mannequin modifications. Earlier than traders rush to dismiss the lawsuit as with out benefit, it should be famous that AAPL’s inventory trades at such a wealthy valuation largely attributable to its fairly monopolistic maintain on its ecosystem. The corporate has not proven sturdy top-line development charges lately, but has persistently commanded an earnings a number of round 30x attributable to Wall Road’s excessive confidence within the ecosystem. As an Apple person myself, I can relate to the notion that the corporate takes clear steps to “lock me in” to the ecosystem, be it via utilizing Apple software program just like the Safari browser and having to make use of the Apple Watch to trace sleep. I additionally should not ignore the notorious “iMessage lock-in” which has apparently contributed partly to bullying in faculties. I might not be stunned if Apple is compelled to regulate these insurance policies which could improve churn charges and finally result in pricing pressures on its gadgets. Whereas I’m of the view that the long-term affect will probably be much less vital than feared, the uncertainty concerning the affect may result in a valuation overhang – the severity of that a number of contractions may weigh on the inventory.

Apple Inventory Key Metrics

In its most up-to-date quarter, AAPL delivered 2% YoY income development, led by 11% development in Companies revenues. The corporate additionally noticed Mac gross sales develop 0.6%, marking a considerable restoration given the phase’s prior onslaught in addition to the truth that the corporate had one much less week as in comparison with the prior yr. As a consequence of share repurchases, earnings per share grew a lot quicker at 16% to $2.18. The corporate ended the quarter with $173 billion in money versus $108 billion in debt, serving to to fund $20 billion in share repurchases. When the inventory was hovering and hovering, traders willingly ignored the usage of capital on share repurchases, however I believe some traders could also be questioning why the corporate continues to repurchase inventory given its relative premium to the market.

On the convention name, administration guided for the following quarter to see fairly muted outcomes, as they are going to now face robust comparables for Mac income development. Administration expects a “related double-digit development charge” for Companies – however like many different tech firms, traders might have to attend a bit longer for any potential tailwinds from generative AI.

Is AAPL Inventory A Purchase, Promote, or Maintain?

At latest costs, AAPL was buying and selling at 27x this yr’s earnings.

Looking for Alpha

That earnings a number of appears to be like lofty on condition that consensus estimates name for single-digit top-line development shifting ahead.

Looking for Alpha

I don’t deny that AAPL continues to commerce at a premium to the broader market. Whereas I’m upgrading the inventory right now, I emphasize that the inventory doesn’t commerce at “pound the desk” sort of costs. That mentioned, I’m lastly of the view that consensus estimates are too conservative as they don’t seem to understand the probability that the corporate advantages from a generative AI supercycle. The corporate was just lately within the information attributable to a report implying that the corporate could also be in discussions with Alphabet Inc. (GOOG) (GOOGL) to permit Gemini to energy generative AI on iPhones. Simply as enterprises internationally have rushed to embrace generative AI capabilities, I anticipate customers to hurry to get generative AI capabilities on their cell gadgets. I’m uncertain that Apple will make these capabilities instantly out there on outdated gadgets (there could also be technological constraints as nicely), that means that customers might probably have to interchange their gadgets with new generative AI-enabled merchandise, which can even carry a hefty price ticket. Along with resulting in a number of years of elevated iPhone earnings, there may be a wave of rising generative AI functions and subscription charges. I anticipate this generative AI increase to greater than offset any affect from the DOJ antitrust lawsuit, because the inventory might ship strong returns even when multiples find yourself contracting some.

What are the important thing dangers? It’s not possible to precisely predict what is going to occur from the DOJ antitrust lawsuit. Maybe the results shall be extra critical than imagined and AAPL might lose its power as a shopper model. It’s doable that the corporate is unable to persuade customers to improve to generative AI-enabled gadgets, or that customers find yourself switching to Android rivals attributable to decrease costs. The inventory continues to closely hinge on sustaining excessive valuation multiples, however that thesis may break down if Wall Road returns to viewing the corporate because it did previous to 2015.

I’m upgrading the inventory to a purchase ranking as I view generative AI to not be priced into the inventory, and think about any pullback associated to the DOJ antitrust lawsuit as a shopping for alternative.

Embrace Rejection! How Getting Denied Saves Us Over $50,000 – Cyber Tech

Zacks Small Cap Analysis – DYAI: Capital Elevate to Speed up Close to Time period Income Progress – Cyber Tech

Philippines accuses China of making an attempt to dam one other vessel – Cyber Tech

About The Author

admin

Azeem Rajpoot, the author behind This Blog, is a passionate tech enthusiast with a keen interest in exploring and sharing insights about the rapidly evolving world of technology. With a background in Blogging, Azeem Rajpoot brings a unique perspective to the blog, offering in-depth analyses, reviews, and thought-provoking articles. Committed to making technology accessible to all, Azeem strives to deliver content that not only keeps readers informed about the latest trends but also sparks curiosity and discussions. Follow Azeem on this exciting tech journey to stay updated and inspired.